Features

How Elliot Rodin was inspired to create a website offering advice on when to take your Canada Pension

By BERNIE BELLAN In 2019 Elliot Rodin happened to read an article about an authoritative U.S. report that provided a detailed analysis showing that 94% of Americans pick the wrong time to begin taking Social Security benefits. Reading about that report led to a shift in Rodin’s life.

Two years after closing down the business (Central Grain) that had been in his family’s hands for over 60 years, Rodin says that he then had time to think about the implications of that US report – and how it could translate into the Canadian scene.

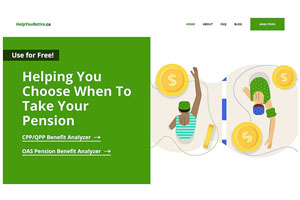

Now, some 15 months after reading about that U.S. report, Rodin has launched a website titled HelpYouRetire.ca.

Long an active member of the Jewish community, Rodin says his most recent involvement in the community was helping to build Oholei Torah Day School at the Jewish Learning Centre in Winnipeg. He says he’s also been on the board of the Shaarey Zedek Synagogue, the Board of Jewish Education, the Winnipeg Jewish Community Council, the Jewish Foundation of Manitoba, and had been a canvasser for the CJA for years, beginning under Ralph Hamovich. He was also a co-chairman of the Operation Exodus campaign.

Still, it’s a long way from running a cattle feed business and volunteering for different Jewish organizations to creating a website intended to help individuals plan their retirement dates.

Using very sophisticated analytical tools, HelpYouRetire.ca allows users to enter information about their age, the age at which they would like to retire, how much they would expect to receive in either CPP/QPP or OAS at a certain age, and how much more they could expect to receive if they were to postpone taking either CPP or OAS by just one year. This financial gain is also shown both as a percentage of future pension proceeds and as a percentage of the annual pension. For a small fee, all of this information can be shown in the “advanced analytics” for all years up to age 69. The information (which can be downloaded) is displayed in bar charts and a numeric chart together with the projected annual pensions.

This information is of great value for anyone thinking about their retirement planning. It can also be very helpful to those who have recently started taking either CPP/QPP or OAS pensions. A little publicized provision of these plans is that within six months of starting to receive one of these pensions, you can reverse your decision by paying back the monies received. In that event, you can take the related pension at a later date. The “advanced analytics” on HelpYouRetire.ca can give you information to assist in making that decision.

But, before we launch into a further exploration of how Elliot Rodin came to be involved in an endeavour that was far removed from selling cattle feed – which was the primary activity of Central Grain, we thought it might be interesting for readers to know something about Rodin’s life. During a long phone conversation we had Rodin told quite an interesting story how he ended up being involved with Central Grain for 60 years – when, had it not been for a fire there in 1966, he probably would have ended up doing something completely different.

While his recent foray into the world of retirement planning might be considered a radical departure for someone who spent so much time in the feed business, when you read about his educational background and his first entry into the business world, you’ll begin to understand how he developed the fine analytical skills that eventually lent themselves to creating HelpYouRetire.ca

Born in 1943, Rodin is the oldest of three children. His earliest years were spent living in his grandparents’ house on Bannerman Avenue, he says, along with his parents and, for a short while, his younger sister, Janis.

“My father (Maurice) was a fruit store proprietor,” Rodin says. “He would be up early in the morning to pick up the fruit. And because we were living at my grandparents’ house, he wasn’t paying any rent, so he was able to save some money. My mother (Lillian) was a university graduate who motivated all her children to work hard and succeed.”

In 1946, an opportunity arose for Rodin’s father to become, with $10,000, a one-third partner in Central Grain, in partnership with the Kanees and the Malchys. “The Malchy who was involved in the partnership died in 1951,” Rodin explains. “My dad and the Kanees bought out his interest and became half partners.

“In 1956, with the assistance of my grandfather, my dad bought out the Kanees and became the sole owner of Central Grain,” Rodin continues. “Soon after that time we moved to the south end – to 431 Queenston.” However, family connections were maintained as Sunday was the day when the whole family would go to the north end to visit relatives.

As a teenager Elliot says that his involvement in the Toppers chapter of BBYO was very important to him. He and his friends learned to organize themselves for a wide range of social, athletic, cultural and fund raising activities.

But, early on he had a taste of the world of business – both in his father’s company and in his own small scale business.

“When I was 16-17 I would go into the office and help with the bookkeeping – and other odd jobs around the place in the summertime,” he explains.

At the same time though, “I had my own business,” he adds. “I had a grass cutting business.” (At that point Rodin tells a story about how one of his customers didn’t want to pay him. Rodin says that he and his friend, Michael Nozick, proceeded to serve a small claims summons against that individual. Apparently, that was Michael Nozick’s first foray into the legal world. By the way, the customer ended up paying Rodin what he was owed.)

In the early 1960s Elliot began a period in his life that saw him acquire a solid education in finance, starting with his obtaining a Bachelor of Commerce degree from the University of Manitoba in 1963.

Rodin continues his story: “I decided I wanted to go away for my MBA degree. I visited three different schools. I took a bus trip – about 43 hours, to Philadelphia, to the Wharton School of Finance, then to Boston, to the Harvard Business School, and then to Ann Arbor, Michigan, to the University of Michigan.

“I had also put my application into Stanford. I wasn’t accepted at Stanford, but I was accepted at Wharton and Michigan, while Harvard said basically ‘We won’t accept you this year because you’re a little young, but we’ll promise you a place in next year’s class.’

“So I decided to wait a year. I worked in the family business for a year, then I went to the Harvard Business School because that was what I thought was the top place to go. I spent two years there and while I was there I also spent one summer with the Skelly Oil Company in Tulsa, Oklahoma.

“I was working on special projects for the treasurer (of Skelly Oil). One of them was a computerized analysis of how to make oil drilling decisions, but it never got off the ground – even though the analysis was very sophisticated, because the exploration people would not accept it because they saw it as infringement on their turf.

“Still, I learned a lot from that particular project. It was my first serious analytical job that had some relationship to the work I was doing at Harvard (and, as Rodin explains later, proved to be of great value in his recent decision to create a website that emphasizes analytical tools.)

“As it turned out, the treasurer at Skelly wanted to hire me when I graduated, but at that time I couldn’t consider working in the States because I would have been drafted. The fact that I was a Canadian wouldn’t have made any difference.

“If I had been a student I wouldn’t get drafted. I also didn’t take any other opportunities that I had in the States. I limited myself to working in Canada.

“I ended up working for six months in Edmonton for a company called the Principal Group. While I worked there I had a lot of diverse responsibilities. I chose all their stocks for a new mutual fund they set up, and designed the text and written material for their first Annual Report. I also did all sorts of analysis for their mortgage operations.

“Then I got the news that the Central Grain plant had been hit by lightning and three-quarters of it had burned down.

“Central Grain was an animal feed processing plant. During the years that my dad was building it up we were basically selling pellet feed for export to the United Kingdom, to Japan, Taiwan. We would load railway cars with pellets, ship them to Thunder Bay, for destinations in the United Kingdom, or ship it to Vancouver for export.

“When this (the fire) happened in 1966, I had to come back to Winnipeg to help my dad settle all the insurance. There were a lot of issues and we rebuilt the plant, but all the key parts of the plant were burned down.

“I decided to settle down in Winnipeg. I took a job with Investors Group, which was similar to what I had in Edmonton. For the first year I was doing special projects, including a report on tax policy. We recommended how life insurance companies should be taxed. (This was before Investors bought Great West Life.) Most of our recommendations were adopted. We were competing with life insurance companies at that time and life insurance companies weren’t paying their fair share of taxes.

“After that year I did some product analyses. Then I started working for the securities department as an analyst. Over a period of time I became a portfolio manager. I ran the Investors international mutual fund. Then I ran the Investors pension accounts. We managed the Hudson’s Bay pension account.

“I was at Investors for 12 years (from 1968-80) and became a vice-president. I left to pursue some independent activities”, but joined Central Grain when it became clear that his dad needed Elliot’s help.

When he joined Central Grain full time in 1980, Rodin began focusing on broadening the markets for the company’s feed pellets. Markets in Western Canada and the United States were cultivated, but he says that he always made sure that the needs of his regular customers were attended to.

“I never took advantage of the fact that there might be a drought in Southern California, for instance, and short my customers in Saskatchewan because I depended on my regular customers for the long haul,” Rodin says.

“I would work long hours if necessary. If a truck came in late and had to be loaded, I would load the truck myself.

Although Central Grain had become a very successful business, Rodin says that the “maximum number of employees we had at one time was no more than 15. We had one truck, but for the most part we hired other trucking companies. We had a machine shop, but the stuff we couldn’t do – we hired other machine shops to do.

“We bought basically the ‘clean-outs’ from grain – all the leftover product. It was all categorized and separated out and properly blended to make different qualities of feed pellets. There was no plant in North America that shipped product as far as we did. We used to ship up to 2,000 miles. Most feed companies ship up to 200 miles.

“The business ran until about three and a half years ago. We were gradually losing customers for reasons that I can’t quite figure out. I needed additional volumes because the company had substantial overhead – for repairs and maintenance.

“So we started to do fuel pellets. We became the second largest manufacturer of fuel pellets in Manitoba – as a substitute for coal, using the same screenings – but the lower quality screenings. The top quality screenings were turned into top quality feed for cattle and bison.

“I was reasonably successful at doing this, but at the end of the day the plant was an old plant. Remember, it was rebuilt in 1966. What was new in 1966 was not new 50 years later. The costs of maintaining the plant to the standards we had to maintain were going up and up.

“Finally, I made the decision that I’m going to have to close it down. I thought: ‘If I can’t make a living at this, then nobody can.’ I decided I’d have to tear the whole place down – and that’s what I did.

“I realized I was getting older and if I didn’t do it I didn’t want to have my children to have the burden of doing it. So, everything that I had built up over 50 years was torn down. I sold whatever equipment that I could, but the rest all went for scrap.

To return to the initial reason for doing this article, Rodin explains his motivation in wanting to create HelpYouRetire.ca. As we already noted, the catalyst was reading about that U.S. report about social security and “that 90% of people in the United States take their pensions at the wrong time.”

He adds though, that “an additional underlying factor in my motivation is that I missed the daily rewards (not the aggravation) that I got from my job running Central Grain. I loved selling and enjoyed my interactions with customers. At the end of the day when I had loaded four big trucks I came home with a feeling of accomplishment. So, I was primed for another challenge where I could get these feelings back. With this website, I am now focusing on marketing where I have to sell myself and the site.”

I asked Rodin whether there was anything in particular in his background that lent itself to the kind of analytical exercise upon which he was to embark.

He answers that “a course that I took at Harvard Business School and the work that I did at Skelly Oil were very relevant to this process.”

I said though “that it sounds like you would need the same background as an actuary” in order to undertake the project into which Rodin has entered.

Rodin agreed, saying “you’re hitting upon a very key point when you say that, but there are a lot actuaries around. Nobody thought of doing what I’m doing.

“I guess part of the answer is most actuaries are fully employed. There aren’t a lot sitting around thinking about what they can do to help Canadians.

“You have to remember that I spent 13 years as a securities analyst and a portfolio manager, so my mind works in a certain way. Nothing that I did at Central Grain though related to this project.”

I asked what were the first steps that Rodin took in developing his website.

He says: “The first steps were that I needed to see whether I could develop the necessary mathematical models to do what I had in mind. Once I had the mathematical models I began working on the structure of a website that would put these mathematical models into practice.

“I was told by various people that setting up a website is not all that difficult.” (Boy, were they ever wrong when it came to this website!)

After an initial contact with someone who was working on their PhD and thought they might be able to produce the kind of website Rodin was looking to create didn’t pan out, a company in Ottawa that had built a similar kind of website agreed to take on the project.

“The idea was that it was going to take a few months” to create the website, Rodin explains.

“But from the time we started up toward the end of February (just before the pandemic hit Canada in full force) it took until the end of August” to finalize the site.

“Every aspect along the way had to be just right – from the mathematics to the functionality. It had to be there so that even people who don’t know much about computers or websites would be able to use this website. Finally, we reached the point where I’m extremely happy with the site.”

So, having read this far, you might ask yourself: “Why should I go to HelpYouRetire.ca?”

So, having read this far, you might ask yourself: “Why should I go to HelpYouRetire.ca?”

It’s quite an easy site to navigate. As has already been explained, simply enter some basic information and the site will provide you with some quick results about how postponing your decision to begin taking either CPP/QPP or OAS by one year will benefit you – or might have benefitted you if you’re already taking your pension.

Then, as Rodin explained, if you’re wanting to know more about how much more your pension would be affected if you decide to wait even longer to begin taking your pension, for a fee you can obtain access to even more comprehensive analytical tools that will show that. The results might surprise you – and it may end up being one of the most important decisions you might ever make with regard to retirement planning.

Features

K-tip placement at Sets on Corydon

Precision K-Tip placement: Where art meets ultimate hair engineering. ✨

Every strand is custom-blended to achieve seamless movement, zero detection, and absolute freedom (yes, even high ponytails on day one). Precision styling takes patience and technical mastery—the result speaks for itself.

.

Features

Israel pavilion ambassadors – then and now

By BERNIE BELLAN Given that Folklorama is on again and the Israel pavilion – Shalom Square, is in full swing, I thought it timely to resurrect an article I first posted to this website in August 2023.

But before reading that article, I wanted you to see who this year’s ambassadors are for Shalom Square:

It was back in 2023, however, that I set out to answer a question that I had asked our readers to help answer: Where was the very first Israel pavilion located? Some readers had thought it was the Golden Age Club, which used to be located on Pritchard and Salter. But others weren’t so sure. Here then is what I wrote back in August 2023 – when, with the help of a librarian at the Winnipeg Public Library, I was able to solve the riddle of where the first Israel pavilion was located:

It was earlier in August 2023 that I had raised a number of questions about the history of the Israel pavilion at Folklorama.

Among those questions were: Where was the first Israel pavilion located and when did the Israel pavilion actually become a permanent fixture in the YMHA on Hargrave (before moving to its current home in the Asper Campus)?

As part of my search for answers to those questions I turned to David Cohen, who had long been the coordinator of the Israel pavilion when it was located on Hargrave, but who didn’t step into that role until 1975.

David thought that the Israel pavilion hadn’t moved to Hargrave until 1974, but he wasn’t sure where the first Israel pavilion had been located.

I tried to find information using the Winnipeg Public Library online digital archive. In case you didn’t know, anyone with a library card can access the library’s online archive. You can also have access to newspaperarchive.com through the library’s digital archive. Newspaperarchive.com is an invaluable reference tool for journalists especially – or anyone wanting to access old newspaper archives, for that matter, but ordinarily you would need a subscription to newspaperarchive.com in order to use it. For some reason, however, the search function in the Winnipeg Public Library’s digital search engine didn’t produce results when I entered the word “Folklorama.”

As a result I called the Winnipeg Public Library for assistance and received great help from someone by the name of Louis-Phillipe. After taking my information, Louis-Phillipe phoned me to say that he had found out that the library had compiled a file of press clippings related to Folklorama going back to the very first year, 1970.

Further, Louis-Phillipe said, he had found a list of the 22 pavilions in that first year of Folklorama, along with where they were located. It turns out that the Israel pavilion was actually located in two different venues that first year: the Rosh Pina and the Shaarey Zedek.

The next day I also heard from reader Phyllis Dana, who confirmed that the Israel Pavilion had been in both synagogues. Phyllis also remembered that the only food served that first year was honey cake.

But the pièce de resistance came when I heard from reader Marilyn Breitman (née Stitz), who now lives in Calgary, when she phoned me on Monday, August 21 (which is when she received the August 16 issue of the paper with my story about Folklorama).

Marilyn told me that, not only did she remember that the first Israel pavilion alternated between the Rosh Pina and the Shaarey Zedek, she had actually been the female representative of the Israel pavilion that first year. Her title, Marilyn said, was simply “Jewish.”

But, as you might also recall, the entire confusion over where the first Israel pavilion was located began with an email I had received from Roz Greenfeld, who had written to correct my mistake when I had written in the August 2 issue that the Israel pavilion had been located in the YMHA from the very beginning.

Roz pointed out that, in 1971, the second year of Folklorama, the Israel pavilion was located in “Council House” or, as it was better known, “The Golden Age Club,” on Pritchard and Salter. How did she remember that? Roz was the female representative of the pavilion that year. Her title, as I found out was “Miss Judea,” she said.

So, if the Israel pavilion was located at both the Rosh Pina and Shaarey Zedek in that first year of Folkorama, and in the Golden Age Club that second year, where was it after that?

It was left to Jewish Heritage Centre of Western Canada archivist Andrew Morrison to come up with the answer to that question. Andrew informed me that the Israel pavilion did indeed move to the YMHA in 1972 and remained there for the next 25 years, until it moved to the Asper Campus in 1997.

There was a further footnote to the story, which is when I decided to try my luck with the Winnipeg Public Library’s online archive one more time. This time, rather than searching for “Folklorama,” I tried searching for old copies of both the Free Press and the Tribune from August 1970. I did manage to get results for the Tribune and when I entered a specific search within the Tribune I found a picture of all the famale representatives of pavilions – in bathing suits.

It turned out – and this was corroborated by both Marilyn Breitman and Roz Greenfeld, the female representatives had to parade in unison – in bathing suits, as part of Folklorama festivities. Each year, as well, a queen of Folklorama was chosen. Neither Marilyn nor Roz was made queen, both of them told me, although Roz was voted “Miss Congeniality.”

In addition to finding out about the early days of the Israel pavilion, I also learned that the Chai dancers were not regular performers at the Israel pavilion in those early years – as they eventually did become. Chai performers would dance only one night in those first years, with other entertainment the other nights.

I did enlist Andrew Morrison’s help once again and did find that Chai performed only one evening during the first few years of Folklorama – from 1970 to 1976. In 1977 Chai began performing every night of Folklorama, but there were other performers on hand as well, including Jerry Maslowsky and Rabbi Yosel Rosenzweig. In 1978 the Chai Folk Ensemble was the featured entertainment every evening; however, a notice that appeared in our paper did say that whistler Harvey Pollock would “be on hand” to entertain – whatever that meant.

While some may wonder of what earth shaking importance all this is, I ask: Isn’t it fun to look back in time – for just a little while, instead of worrying about more immediate problems, such as global warming, inflation, terrorist attacks in Israel, and whether Donald Trump will be president while he’s in jail?

Features

EINSTEIN, RITA AND ME

By DAVID R. TOPPER In the early 1960s, when I was an undergraduate student majoring in Physics at Duquesne University in Pittsburgh – there was only one girl in my advanced physics classes. As I learned later, nothing much had changed since the days of Einstein. When he was studying Physics at the Polytechnic in Zurich, the physics classes were all male – except for Mileva Marić, a Serbian who was the first girl in high school ever to take a physics course in the entire Austro-Hungarian Empire. Because Switzerland was the only place where women were admitted to university classes, she was there with Albert in Zurich.

She was very smart, especially in math, and also proficient at the piano. Born with a dislocated hip, Mileva had a slight limp, and the men in the class ignored her – except for one, Albert. They became a couple and eventually married.

Back to me in my university physics classes – where it seems that little had changed for over sixty years. In my advanced classes there was only one girl. Her name was Rita. She mainly stayed to herself. Majoring in Mathematics, she took all the advanced physics courses available, right through the fourth year. In short, in those predominantly male classes, she was an anomaly – alone and ignored by her classmates.

Except me. No, I didn’t date her, yet I didn’t ignore her. During those undergraduate years, I lived at home and took a bus or a trolley to school five days a week, leaving early in the morning. The university is in downtown Pittsburgh. Walking to the campus, I first went to the Physics Department, using it as my base. From there I went to my other classes during the day. There was a small classroom in the Department that was almost always empty, especially in the morning. It could be used for individual studying or small group discussions and such. In the early morning, I was usually the only one there – except for Rita, who used it for studying, too. She often was there, even before me. Usually the conversation started by me saying something like: “Hi Rita, did you get the last problem in mechanics class homework?” Her response was invariably, “Yes.” We would go over it, with her finding my mistakes. We had an amiable relationship that never went beyond our interactions about physics – right up to the end of our university years. As far as I can remember, I don’t think I knew much about her beyond the classroom.

But one event, which I’ll never forget, stands out. It was during our last year of classes in a course on the theory of relativity. For the textbook the prof used a paperback edition of the original papers on the theory. Early in the course, we went through Einstein’s first paper of 1905 – step by step. On this particular day, the prof came in and said he had a problem with the next step in the paper. As we all sat with our books in front of us, he pointed to a certain equation where we ended in the previous class. In the next sentence, Einstein says that such and such follows. The problem for the prof was that he didn’t know how Einstein got that deduction. I looked at it, and didn’t have a clue either.

Just then, Rita’s hand went up. She said she thinks she knows how Einstein got it. The prof asked her to come up to the blackboard and show him. Rita did, and the prof said that she was right. I’m quite sure that – then and there – Rita got an A in that course, if not an A+.

That gives you some idea about Rita and my relationship with her at the time. Not a very significant part of my 4-year undergraduate years – except for this one event in a physics course.

Why then am I bringing this up now, so many years later? Here’s why.

I graduated with my BS degree in the fall of 1964. I then went to graduate school at Case Institute of Technology in Cleveland, majoring in Physics. (It’s now Case-Western Reserve University.)

When I moved there, I lived in a formerly swanky hotel on the edge of the campus, which was purchased by the university as a residence solely for graduate students. They called it The Graduate House. Eleven floors, the top 8 with suites for students, with one floor solely for female students. It was a radical experiment in co-ed living for the time.

My first day there, after getting my room and putting my things in drawers and so forth, it was late in the afternoon – and I was hungry. I had been told when I registered that the dining hall would open the following morning, but for now there was no food. However, on the third floor there were vending machines with sandwiches and such, so I went to find them.

Going down the elevator, exiting at the third floor, and walking down a hall – suddenly I heard my name called. “David, what are you doing here?” Turning around – there was Rita! It was quite a surprise for both of us. This tells you how minimally we interacted before; not even knowing that we both were going to the same graduate school.

I told her that I was majoring in Physics at Case. She, of course, was majoring in Math. After a chat about all this, I said that I was looking for the sandwich machines. She said that there was a diner nearby, and she was going there for dinner with someone else she had just met so I went, too. Thus, Rita and I reunited in Cleveland, now living in the same building.

In a short while, I made friends with a group of people in the Graduate House with diverse majors. Some were in various sciences, others in humanities. It was a lively group, with animated discussions on a range of academic topics, including politics, especially as the Vietnam War became the center of the news in the USA.

Rita was not a part of that group, but I did often see her. Being the eager student that I was, I was up early, getting to the university to study in the library before classes started. Coming to the dining room for breakfast, not long after it opened, I often saw Rita, too – all alone in a far corner. I took my tray and we had breakfast together. Except for that morning ritual, I seldom had any interactions with her.

Thinking about this now, I find the parallel morning rituals (first in Pittsburgh and then in Cleveland) a fascinating serendipitous episode in my life. The difference was that in Cleveland, we were not taking the same courses so we didn’t have to compare solutions to homework. We did talk about our respective courses, and interestingly a parallel appeared. By around mid-term of that first year in graduate school, we both were less than enthusiastic about what we were learning and, accordingly, were both thinking of not carrying on in our respective subjects.

For me it was Quantum Mechanics and the impossibility for us to know reality in itself. Everything was statistical, uncertain and almost esoteric. I found the uncritical attitude toward this world-view to be almost religious in nature. (I only learned later that Einstein felt the same way!)

For Rita, it was the same, despite the different fields. The math now was far beyond basic geometry, algebra and calculus. Topology, Group Theory, Galois’ Theory, and more – all culminating in Gödel’s Theorem, which asserts that all mathematical knowledge is inherently incomplete. It all was too esoteric for her. She knew that she was not going to get a PhD in mathematics.

We commiserated together, with another parallel in our unusual relationship, but with a difference. I still wanted to get my Master’s Degree and somehow still go on to get a job as a professor – that had been my goal in life ever since my first semester at Duquesne. Rita, however, was thinking of dropping out immediately and leaving university life altogether.

For me, this problem was resolved in my second year of Physics at Case, when I took a course taught by Martin Klein. Although he was a physicist in the Department, for many years he no longer was doing research in it. Instead, he was writing papers on the history of the subject – mainly involving Einstein, Boltzmann, Gibbs, Ehrenfest and others. Today those papers are paragons in the field. It was my extremely good luck that the department permitted him to teach such material for the first time.

I loved the course. I was enthralled by the topics – this was the way I wanted to learn physics, through its history. After getting my Master’s in Physics at the end of that year, I moved across campus to the History of Science Department. In another four years I had a PhD in the subject.

Back to early 1965: I tried to talk Rita out of dropping out, but she was adamant. The kicker was this: she really preferred numbers with $$$$ in front of them. Yes, she wanted to be an accountant. She didn’t want to waste any more time here, when she could be home getting her accounting credentials. As I recall, sometime before the spring of that year she went back to Pittsburgh. I’m sure she had an easy time getting her accounting licence and all that went with it. As she was very smart. My guess is that she was an excellent accountant and was very successful in that career.

I have no way of knowing. We didn’t keep in touch (honestly, I don’t know why not) and I can’t even remember her last name. All that I can recall is what I’ve written here. Nonetheless, I find these two interactions between Rita and me an interesting and pleasing tidbit about life and relationships – so much so that I deem it worthy of repeating here.

David R. Topper writes in Winnipeg, Canada. His work has appeared in Mono, Poetic Sun, Discretionary Love, Poetry Pacific, Academy of the Heart & Mind, Altered Reality Mag. and elsewhere.

His poem Seascape with Gulls: My Father’s Last Painting won first prize in the annual poetry contest of CommuterLit Mag – May 12, 2025.