Features

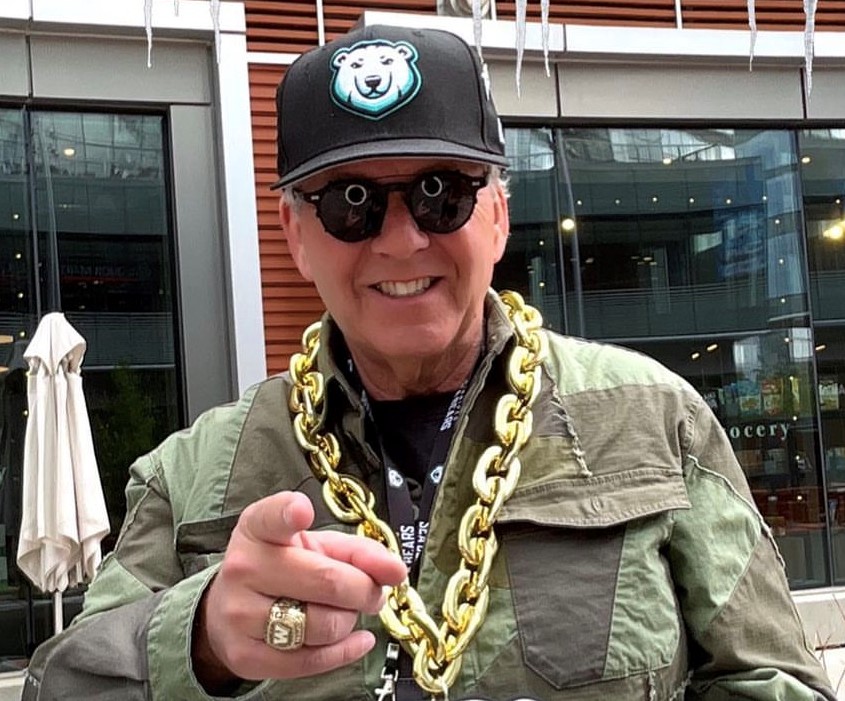

David Asper has brought excitement to a new generation of basketball fans with the Winnipeg Sea Bears

By BERNIE BELLAN

June 8, 2023 The name David Asper has long been associated with Winnipeg sports teams.

A former Chair of the Winnipeg Blue Bombers – and someone who achieved both notoriety for how directly involved he became with that team – even going so far as to invade the locker room after a particularly brutal loss (only to be pushed out by now CEO Wade Miller), Asper was also involved with a pro basketball team known as the Winnipeg Thunder, which played here from 1992-94.

This past year, however, Asper took another foray into sports at the ownership level with Winnipeg’s newest sports franchise, the Winnipeg Sea Bears.

The Sea Bears play in a summer league – which is also when the Winnipeg Thunder, a team in which Asper also had an owership stake played. (Another team, the Winnipeg Cyclone, owned by Earl Barish, played in the winter.),

The Sea Bears franchise is the newest addition to what is now a 10-team All Canadian league known as the Canadian Elite Basketball League. So far, by any measure, the team is off to a roaring start.

Recently I chatted with Asper about what led him to enter – again, into the risky world of professional sports and why he’s confident that this time around, the Sea Bears and the league they play in, will be lasting successes.

I began by asking him whether he’s pleased with the attendance at Sea Bears games thus far? (At the time of our conversation the team had played five home games, with an average attendance over 4,000 each game.)

“Yes, I’m very pleased with the reception we’ve gotten so far,” Asper said, “but it’s my nature – it’s the entrepreneur’s curse, to be very cautious about it, because when we began – when you start a business – any business, you never know whether anyone’s going to actually show up and, if they do, whether they’ll keep coming back.”

I suggested to Asper that the history of pro basketball teams in Winnipeg is less than impressive, but he responded that the Winnipeg Thunder actually did “very well,” but “both leagues that the team was affiliated with collapsed.”

“The Thunder played in the summer. The Cyclone played in the winter. I had a better perspective of seeing what would happen if you played in the summer – which is what appealed to me about this league,” Asper added.

I asked, “How far back in time did your planning for the Sea Bears begin?”

Asper said he “started in the spring of ’22, spent time all last summer going across country to games, and then I decided I really liked what I was seeing. I was concerned about the show – the competitiveness of the basketball – and I’m not a basketball person, but I think I have a sense of when something is entertaining and athletic.

“By mid-summer we thought we were going to go for it, we had some negotiation with the league, and we were finally able to announce – late, relatively speaking, at the end of November. We put ourselves in quite a time crush being able to launch for 2023 because training camp starts mid-May, so we only had five months really. We had to hire staff, get tickets out and get ourselves prepared, so it’s been a very hectic time.”

I said to Asper that I wasn’t all that familiar with the Canadian Elite Basketball League and he did give me some of the league’s history, but after the interview I dug deeper into the league’s history.

The CEBL is now in its fifth season, having begun in the summer of 2019, originally with six teams, which were all owned by the league. It now has ten teams in two divisions, from six different provinces:The east division is made up of one team in Quebec (in Montreal), and four in Ontario (in Brampton, Niagara, Ottawa, and Scarborough); and a west division: one in Manitoba (the Sea Bears), one in Saskatchewan (in Saskatoon); two in Alberta (in Calgary and Edmonton), and one in BC (in Langley).

While five of the teams are still owned by the league, there are now five private owners – in Langley, Calgary, Edmonton, and Scarborough, in addition to Asper in Winnipeg.

For the most part the teams play in smaller venues, with the exception of the Sea Bears, who play in Canada Life Centre, which can hold over 15,000 (although seating is confined to the lower level).

Another difference between the CEBL and other leagues that have come and gone in Canada is the heavy emphasis on Canadian players on each team. As Asper explained, each team has 10 players, of whom six have to be Canadian, three can be American, and a tenth can be international.

“We collaborate with Basketball Canada,” Asper observed, and it is a great opportunity for Canadian university players to hone their skills.

Not only that, Asper added that “last year nine players coming out of our league signed NBA contracts,” which gives you an idea what a high level of basketball is played in the CEBL.

According to Wikipedia, each team operates under a salary cap of only $8,000 per team per game. (There are 20 regular games, followed by a round robin playoff tournament modeled on the NCAA Final Four tournament.)

I asked Asper about what I described as his “abiding interest in sports,” given his history of involvement with both pro basketball and football teams.

He said that he thinks “sport is an important part of culture.”

“Where does it come from?” I asked.

“Well, I played sports as a kid,” Asper answered. “I didn’t play basketball, but I’ve seen the power of sports to be inclusive, to be inspirational, to be a shared common experience. I believe very strongly – I know that others in the arts community will dispute it, but I believe sports is as integral to culture as is art and other forms of activities.”

I asked Asper about the role he played in the building of IG Field (where the Blue Bombers now play).

He said that it was never his idea to build a new stadium at the University of Manitoba.

“My plan was to build it at Polo Park and I had everyone lined up and agreed to build it there. I don’t know what happened. I had led the whole project and Greg Selinger wound up taking it over.

I remarked: “Oh yah, I remember, there was an election.”

Turning back to the Sea Bears, I observed that, from pictures in the paper and what I had seen on TV, the team has been drawing a much younger crowd than say the Bombers or Jets – and a far more diverse crowd ethnically. I asked Asper whether that was part of the plan when he thought of starting a basketball team here.

He said, “The answer is yes. When I went across the country last summer and went to games and talked to fans, you could visibly see who was there and a lot of them were young families. There were also grandparents – people my age. It was a broader demographic than I thought it would be. I think that seeing young people at a game is very appealing to a broad age demography, but Bernie, when I would talk to first or second generation Canadians at those games, these were not people who grew up with hockey or football, but for them – basketball – when I talked about shared common experience and shared culture, I’m talking about these families – these new Canadians, meeting with legacy, old Canadians and having a shared common experience as Canadians that was so heart-warming. I said: ‘I want to be part of this.’

“It may be relatively small compared to football and hockey, but it’s doing a service. It’s serving a larger purpose, and what we’ve seen at the games so far – and it really overwhelms me, is that’s exactly what’s happening in Winnipeg.”

“I was talking to kids at the last game – they were part of two youth groups, who had never been to Canada Life Centre and came for the first time to a basketball game – and it blew their minds. They could not believe how great this was – predominantly new Canadians.”

I asked what the ticket price structure is?

Asper said, “They start at roughly 20 bucks. We try to have an entry point for families that’s very accessible.”

I asked whether Ruth (David’s wife) is involved with the team (since she was pictured seated along side David at the first game)?

Asper said, “No, but she’s the team’s number 2 fan.” He also told me that Ruth has a very strong background herself in sports.

I said that I remembered when she was co-owner of Tights, along with other fitness centers in Winnipeg over the years.

Asper said, “Not only that, but Ruth was the trainer for the (University of Manitoba) Bisons football team and she was the trainer for the Churchill Bulldogs football team. She’s in the Churchill Bulldogs Hall of Fame. She really has an experiential perspective on sports. She’s not involved, but she certainly knows the owner – let’s put it that way.”

I wondered about the stability of this particular basketball league – given the past failures of other basketball leagues that had Winnipeg franchises.

“Have there been any teams that have dropped out since the league started five years ago?” I asked.

“There was a team in Newfoundland, and it dropped out,” Asper answered. “Other teams have moved to different markets, so Hamilton moved to Brampton, Guelph had a team that moved to Calgary – which was important because that created a west and an east division. The league has seen unparalleled success this year. The growth in the league is really quite remarkable.”

Asper also noted that “We’re trying to build a sustainable summer event, so it takes a significant investment to start a team up, but the owners who are either starting or acquiring franchises are very committed to investing and growing. The league itself has come through its start-up anarchy, which is always the case in a start-up anything and now it’s moving into scaling up – because it’s working. People want to see this product.”

He also observed that the league is very competitive. Because it’s such a short season (only 20 games), “every single game matters.”

Asper explained that “we have a unique ending to the games” (in the CEBL). “Instead of the clock just running out – like you’d see in an NBA game, where you’d see them try to manage the clock, where the team that’s winning will try to run out the clock and the team that’s losing will try to create fouls and slow it down, what we do is, at the first stoppage in play with close to four minutes left to go in the game we create what’s called a ‘target score,’ so we add nine to the leading team’s score, so that, for example, the score is 84-80, then we turn off the clock, and the first team to 93 wins.

“So, not only does every game matter, the way the games end are so exciting that people leave feeling exhilarated or demoralized. There’s a really emotional way that our games end that really creates a compelling fan experience.”

I asked: “Anything else you want to add?”

Asper said: “Get your tickets at seabears.ca!”

Features

Israel pavilion ambassadors – then and now

By BERNIE BELLAN Given that Folklorama is on again and the Israel pavilion – Shalom Square, is in full swing, I thought it timely to resurrect an article I first posted to this website in August 2023.

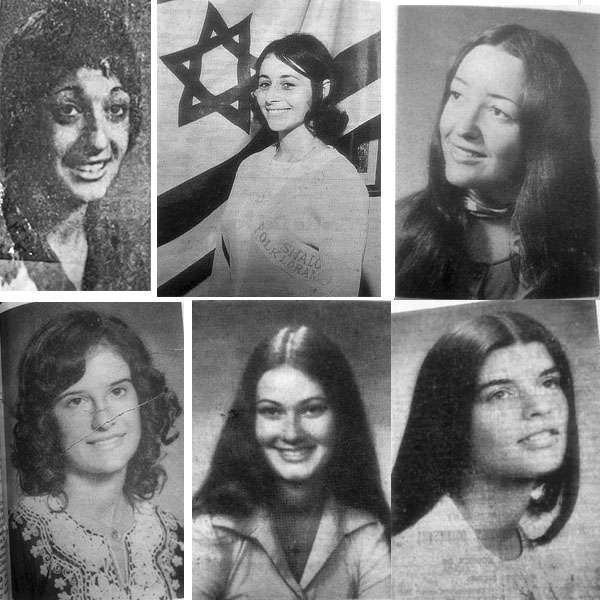

But before reading that article, I wanted you to see who this year’s ambassadors are for Shalom Square:

It was back in 2023, however, that I set out to answer a question that I had asked our readers to help answer: Where was the very first Israel pavilion located? Some readers had thought it was the Golden Age Club, which used to be located on Pritchard and Salter. But others weren’t so sure. Here then is what I wrote back in August 2023 – when, with the help of a librarian at the Winnipeg Public Library, I was able to solve the riddle of where the first Israel pavilion was located:

It was earlier in August 2023 that I had raised a number of questions about the history of the Israel pavilion at Folklorama.

Among those questions were: Where was the first Israel pavilion located and when did the Israel pavilion actually become a permanent fixture in the YMHA on Hargrave (before moving to its current home in the Asper Campus)?

As part of my search for answers to those questions I turned to David Cohen, who had long been the coordinator of the Israel pavilion when it was located on Hargrave, but who didn’t step into that role until 1975.

David thought that the Israel pavilion hadn’t moved to Hargrave until 1974, but he wasn’t sure where the first Israel pavilion had been located.

I tried to find information using the Winnipeg Public Library online digital archive. In case you didn’t know, anyone with a library card can access the library’s online archive. You can also have access to newspaperarchive.com through the library’s digital archive. Newspaperarchive.com is an invaluable reference tool for journalists especially – or anyone wanting to access old newspaper archives, for that matter, but ordinarily you would need a subscription to newspaperarchive.com in order to use it. For some reason, however, the search function in the Winnipeg Public Library’s digital search engine didn’t produce results when I entered the word “Folklorama.”

As a result I called the Winnipeg Public Library for assistance and received great help from someone by the name of Louis-Phillipe. After taking my information, Louis-Phillipe phoned me to say that he had found out that the library had compiled a file of press clippings related to Folklorama going back to the very first year, 1970.

Further, Louis-Phillipe said, he had found a list of the 22 pavilions in that first year of Folklorama, along with where they were located. It turns out that the Israel pavilion was actually located in two different venues that first year: the Rosh Pina and the Shaarey Zedek.

The next day I also heard from reader Phyllis Dana, who confirmed that the Israel Pavilion had been in both synagogues. Phyllis also remembered that the only food served that first year was honey cake.

But the pièce de resistance came when I heard from reader Marilyn Breitman (née Stitz), who now lives in Calgary, when she phoned me on Monday, August 21 (which is when she received the August 16 issue of the paper with my story about Folklorama).

Marilyn told me that, not only did she remember that the first Israel pavilion alternated between the Rosh Pina and the Shaarey Zedek, she had actually been the female representative of the Israel pavilion that first year. Her title, Marilyn said, was simply “Jewish.”

But, as you might also recall, the entire confusion over where the first Israel pavilion was located began with an email I had received from Roz Greenfeld, who had written to correct my mistake when I had written in the August 2 issue that the Israel pavilion had been located in the YMHA from the very beginning.

Roz pointed out that, in 1971, the second year of Folklorama, the Israel pavilion was located in “Council House” or, as it was better known, “The Golden Age Club,” on Pritchard and Salter. How did she remember that? Roz was the female representative of the pavilion that year. Her title, as I found out was “Miss Judea,” she said.

So, if the Israel pavilion was located at both the Rosh Pina and Shaarey Zedek in that first year of Folkorama, and in the Golden Age Club that second year, where was it after that?

It was left to Jewish Heritage Centre of Western Canada archivist Andrew Morrison to come up with the answer to that question. Andrew informed me that the Israel pavilion did indeed move to the YMHA in 1972 and remained there for the next 25 years, until it moved to the Asper Campus in 1997.

There was a further footnote to the story, which is when I decided to try my luck with the Winnipeg Public Library’s online archive one more time. This time, rather than searching for “Folklorama,” I tried searching for old copies of both the Free Press and the Tribune from August 1970. I did manage to get results for the Tribune and when I entered a specific search within the Tribune I found a picture of all the famale representatives of pavilions – in bathing suits.

It turned out – and this was corroborated by both Marilyn Breitman and Roz Greenfeld, the female representatives had to parade in unison – in bathing suits, as part of Folklorama festivities. Each year, as well, a queen of Folklorama was chosen. Neither Marilyn nor Roz was made queen, both of them told me, although Roz was voted “Miss Congeniality.”

In addition to finding out about the early days of the Israel pavilion, I also learned that the Chai dancers were not regular performers at the Israel pavilion in those early years – as they eventually did become. Chai performers would dance only one night in those first years, with other entertainment the other nights.

I did enlist Andrew Morrison’s help once again and did find that Chai performed only one evening during the first few years of Folklorama – from 1970 to 1976. In 1977 Chai began performing every night of Folklorama, but there were other performers on hand as well, including Jerry Maslowsky and Rabbi Yosel Rosenzweig. In 1978 the Chai Folk Ensemble was the featured entertainment every evening; however, a notice that appeared in our paper did say that whistler Harvey Pollock would “be on hand” to entertain – whatever that meant.

While some may wonder of what earth shaking importance all this is, I ask: Isn’t it fun to look back in time – for just a little while, instead of worrying about more immediate problems, such as global warming, inflation, terrorist attacks in Israel, and whether Donald Trump will be president while he’s in jail?

Features

EINSTEIN, RITA AND ME

By DAVID R. TOPPER In the early 1960s, when I was an undergraduate student majoring in Physics at Duquesne University in Pittsburgh – there was only one girl in my advanced physics classes. As I learned later, nothing much had changed since the days of Einstein. When he was studying Physics at the Polytechnic in Zurich, the physics classes were all male – except for Mileva Marić, a Serbian who was the first girl in high school ever to take a physics course in the entire Austro-Hungarian Empire. Because Switzerland was the only place where women were admitted to university classes, she was there with Albert in Zurich.

She was very smart, especially in math, and also proficient at the piano. Born with a dislocated hip, Mileva had a slight limp, and the men in the class ignored her – except for one, Albert. They became a couple and eventually married.

Back to me in my university physics classes – where it seems that little had changed for over sixty years. In my advanced classes there was only one girl. Her name was Rita. She mainly stayed to herself. Majoring in Mathematics, she took all the advanced physics courses available, right through the fourth year. In short, in those predominantly male classes, she was an anomaly – alone and ignored by her classmates.

Except me. No, I didn’t date her, yet I didn’t ignore her. During those undergraduate years, I lived at home and took a bus or a trolley to school five days a week, leaving early in the morning. The university is in downtown Pittsburgh. Walking to the campus, I first went to the Physics Department, using it as my base. From there I went to my other classes during the day. There was a small classroom in the Department that was almost always empty, especially in the morning. It could be used for individual studying or small group discussions and such. In the early morning, I was usually the only one there – except for Rita, who used it for studying, too. She often was there, even before me. Usually the conversation started by me saying something like: “Hi Rita, did you get the last problem in mechanics class homework?” Her response was invariably, “Yes.” We would go over it, with her finding my mistakes. We had an amiable relationship that never went beyond our interactions about physics – right up to the end of our university years. As far as I can remember, I don’t think I knew much about her beyond the classroom.

But one event, which I’ll never forget, stands out. It was during our last year of classes in a course on the theory of relativity. For the textbook the prof used a paperback edition of the original papers on the theory. Early in the course, we went through Einstein’s first paper of 1905 – step by step. On this particular day, the prof came in and said he had a problem with the next step in the paper. As we all sat with our books in front of us, he pointed to a certain equation where we ended in the previous class. In the next sentence, Einstein says that such and such follows. The problem for the prof was that he didn’t know how Einstein got that deduction. I looked at it, and didn’t have a clue either.

Just then, Rita’s hand went up. She said she thinks she knows how Einstein got it. The prof asked her to come up to the blackboard and show him. Rita did, and the prof said that she was right. I’m quite sure that – then and there – Rita got an A in that course, if not an A+.

That gives you some idea about Rita and my relationship with her at the time. Not a very significant part of my 4-year undergraduate years – except for this one event in a physics course.

Why then am I bringing this up now, so many years later? Here’s why.

I graduated with my BS degree in the fall of 1964. I then went to graduate school at Case Institute of Technology in Cleveland, majoring in Physics. (It’s now Case-Western Reserve University.)

When I moved there, I lived in a formerly swanky hotel on the edge of the campus, which was purchased by the university as a residence solely for graduate students. They called it The Graduate House. Eleven floors, the top 8 with suites for students, with one floor solely for female students. It was a radical experiment in co-ed living for the time.

My first day there, after getting my room and putting my things in drawers and so forth, it was late in the afternoon – and I was hungry. I had been told when I registered that the dining hall would open the following morning, but for now there was no food. However, on the third floor there were vending machines with sandwiches and such, so I went to find them.

Going down the elevator, exiting at the third floor, and walking down a hall – suddenly I heard my name called. “David, what are you doing here?” Turning around – there was Rita! It was quite a surprise for both of us. This tells you how minimally we interacted before; not even knowing that we both were going to the same graduate school.

I told her that I was majoring in Physics at Case. She, of course, was majoring in Math. After a chat about all this, I said that I was looking for the sandwich machines. She said that there was a diner nearby, and she was going there for dinner with someone else she had just met so I went, too. Thus, Rita and I reunited in Cleveland, now living in the same building.

In a short while, I made friends with a group of people in the Graduate House with diverse majors. Some were in various sciences, others in humanities. It was a lively group, with animated discussions on a range of academic topics, including politics, especially as the Vietnam War became the center of the news in the USA.

Rita was not a part of that group, but I did often see her. Being the eager student that I was, I was up early, getting to the university to study in the library before classes started. Coming to the dining room for breakfast, not long after it opened, I often saw Rita, too – all alone in a far corner. I took my tray and we had breakfast together. Except for that morning ritual, I seldom had any interactions with her.

Thinking about this now, I find the parallel morning rituals (first in Pittsburgh and then in Cleveland) a fascinating serendipitous episode in my life. The difference was that in Cleveland, we were not taking the same courses so we didn’t have to compare solutions to homework. We did talk about our respective courses, and interestingly a parallel appeared. By around mid-term of that first year in graduate school, we both were less than enthusiastic about what we were learning and, accordingly, were both thinking of not carrying on in our respective subjects.

For me it was Quantum Mechanics and the impossibility for us to know reality in itself. Everything was statistical, uncertain and almost esoteric. I found the uncritical attitude toward this world-view to be almost religious in nature. (I only learned later that Einstein felt the same way!)

For Rita, it was the same, despite the different fields. The math now was far beyond basic geometry, algebra and calculus. Topology, Group Theory, Galois’ Theory, and more – all culminating in Gödel’s Theorem, which asserts that all mathematical knowledge is inherently incomplete. It all was too esoteric for her. She knew that she was not going to get a PhD in mathematics.

We commiserated together, with another parallel in our unusual relationship, but with a difference. I still wanted to get my Master’s Degree and somehow still go on to get a job as a professor – that had been my goal in life ever since my first semester at Duquesne. Rita, however, was thinking of dropping out immediately and leaving university life altogether.

For me, this problem was resolved in my second year of Physics at Case, when I took a course taught by Martin Klein. Although he was a physicist in the Department, for many years he no longer was doing research in it. Instead, he was writing papers on the history of the subject – mainly involving Einstein, Boltzmann, Gibbs, Ehrenfest and others. Today those papers are paragons in the field. It was my extremely good luck that the department permitted him to teach such material for the first time.

I loved the course. I was enthralled by the topics – this was the way I wanted to learn physics, through its history. After getting my Master’s in Physics at the end of that year, I moved across campus to the History of Science Department. In another four years I had a PhD in the subject.

Back to early 1965: I tried to talk Rita out of dropping out, but she was adamant. The kicker was this: she really preferred numbers with $$$$ in front of them. Yes, she wanted to be an accountant. She didn’t want to waste any more time here, when she could be home getting her accounting credentials. As I recall, sometime before the spring of that year she went back to Pittsburgh. I’m sure she had an easy time getting her accounting licence and all that went with it. As she was very smart. My guess is that she was an excellent accountant and was very successful in that career.

I have no way of knowing. We didn’t keep in touch (honestly, I don’t know why not) and I can’t even remember her last name. All that I can recall is what I’ve written here. Nonetheless, I find these two interactions between Rita and me an interesting and pleasing tidbit about life and relationships – so much so that I deem it worthy of repeating here.

David R. Topper writes in Winnipeg, Canada. His work has appeared in Mono, Poetic Sun, Discretionary Love, Poetry Pacific, Academy of the Heart & Mind, Altered Reality Mag. and elsewhere.

His poem Seascape with Gulls: My Father’s Last Painting won first prize in the annual poetry contest of CommuterLit Mag – May 12, 2025.

Features

Best Online Casinos Canada (2026) – Trusted Real Money Sites For Canadian Players

A great casino experience goes beyond winning; it’s about fast, secure payouts and reliable service. After reviewing dozens of sites, our top picks for Canadian players are Wild Tokyo, Lucky7, Slots Gallery, Boho Casino, and BitStarz, selected for their payouts, bonuses, security, and overall value.

Top 5 Best Online Casinos Canada Rankings

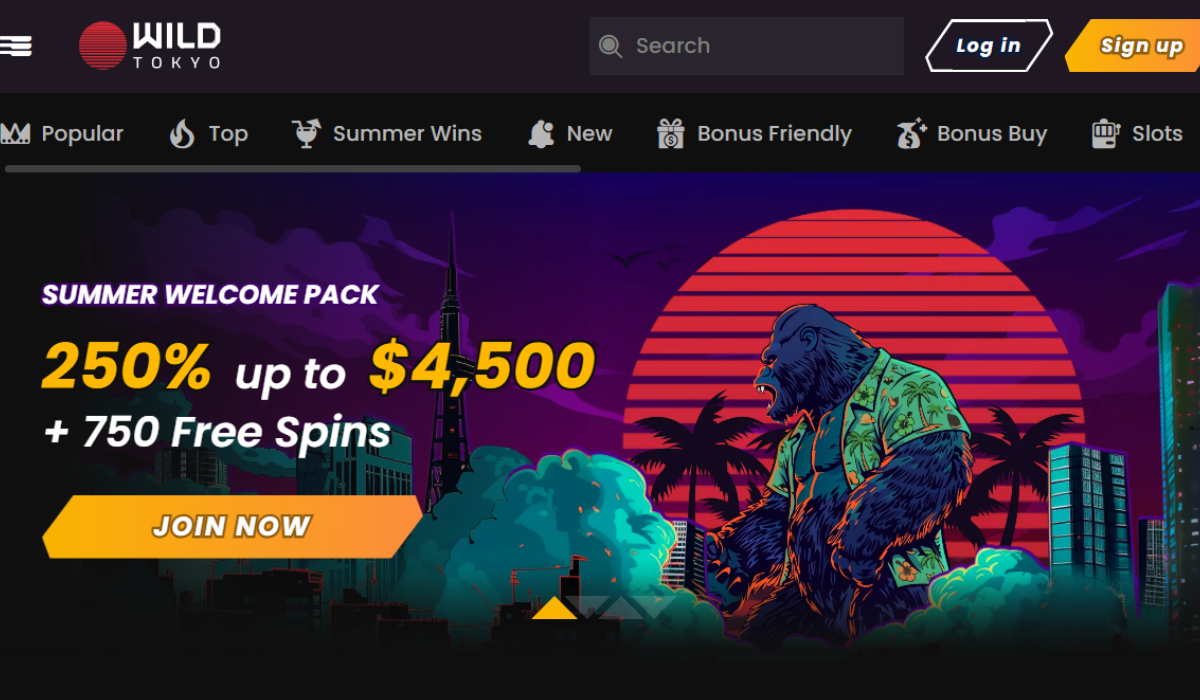

1️⃣ Wild Tokyo – 250% Up to C$4,500 + 750 Free Spins ✅️

2️⃣ Lucky7 – Up to C$3,000 + 200 Free Spins ✅️

3️⃣ Slots Gallery – Up to C$9,750 + 225 Free Spins ✅️

4️⃣ Boho Casino – Up to C$9,750 + 225 Free Spins ✅️

5️⃣ BitStarz – 300% up to C$2,000 or 5 BTC + 180 Free Spins ✅️

What Makes the Best Online Casinos Canada Stand Out?

The best online casinos Canada offer more than large bonuses. They combine fast withdrawals, secure payment methods, quality game libraries, mobile-friendly gaming, fair terms, and reliable support. With Canadian players increasingly seeking faster verification, smooth CAD transactions, and features like Megaways slots and live dealer games, security, payment reliability, and transparent promotions remain key factors when choosing among the best Canadian online casinos.

Based on these factors, our review highlights five of the best online casinos Canada that stand out for different strengths, helping readers find a reliable casino based on their preferences.

- Wild Tokyo: Best for high-roller rewards.

- Lucky7: Best for flexible bonuses.

- Slots Gallery: Best for slot variety.

- Boho Casino: Best for bonus offers.

- BitStarz: Best for crypto gaming.

Key Criteria for Rating Canadian Online Casinos

Before choosing a casino for real money gaming, it is important to review factors that influence safety, reliability, and overall value. The best online casinos Canada provide secure payments, fair gaming practices, and transparent policies, making them stronger choices for anyone searching for a trusted online casino Canada experience.

- Licensing & Regulation

Many offshore casinos operate under licences such as Curaçao, which provide regulatory oversight, although Canadian players should review individual casino terms and policies. This is an important factor when comparing the best Canadian online casinos.

- Banking Efficiency

The best online casinos for real money provide secure payment options, including e-wallets and cryptocurrency methods, allowing Canadian players to manage transactions with confidence.

- Game Fairness

Independent audits from organisations such as eCOGRA and iTech Labs help verify Random Number Generator (RNG) systems, ensuring fair results across casino games and supporting a trustworthy gaming experience.

- Bonuses & Terms

The best online real money casino choices also focus on clear bonus rules, reasonable wagering requirements, and transparent promotions that deliver long-term value.

In-Depth Reviews of the Best Online Casinos Canada

Our expert reviews of the best online casinos Canada examine bonuses, payment options, game variety, security, and reliability to help readers find trusted casinos for real money gaming.

1. Wild Tokyo: Best Online Casino Canada For Game Variety

Wild Tokyo stands out among the best online casinos Canada for users who value a wide selection of casino games and a flexible gaming experience. Our experts reviewed its overall design, game categories, promotional options, and mobile usability to understand how it performs as a modern best online casino Canada choice.

The casino offers a balanced mix of online slots, jackpot games, table games, and live dealer entertainment. This makes it suitable for users searching for the best online casino Canada real money experience that provides more than one type of gameplay. Instead of focusing on a single category, Wild Tokyo allows users to explore different styles from one account.

For users comparing Canadian online casinos, Wild Tokyo provides a simple browsing experience with easy access to games, promotions, and account features. Its mobile-friendly design also allows users to enjoy casino entertainment through smartphones and tablets without requiring additional software downloads.

Welcome Bonus & Promotions

- Welcome Bonus: 250% up to C$4,500 + 750 Free Spins

- Matchday High Roller Bonus: 110% up to C$2,300 + 270 FS + 3 Coins

- Weekly Bonus: 40% up to C$300

- Daily VIP Cashback: 7%

Key Features

- Large selection of online casino games

- Strong focus on slot variety

- Live dealer entertainment options

- Mobile browser compatibility

- Regular promotional campaigns

- Easy navigation between games and account sections

Our Verdict

Wild Tokyo earned recognition in our review of the best online casinos Canada because it combines variety, accessibility, and convenience in one casino experience. Its extensive game selection makes it appealing for users who enjoy switching between slots, table games, and live dealer options.

For anyone searching for the best online real money casino with a broad entertainment selection, Wild Tokyo provides a well-rounded choice with strong gaming variety and flexible features.

2. Lucky7: Best Canadian Online Casino For Promotions & Banking Flexibility

Lucky7 offers a balanced casino experience with a strong focus on promotions, game variety, and flexible payment options. During our review of the best online casinos Canada, our experts analysed how Lucky7 performs across important areas such as bonuses, game accessibility, account usability, and banking features.

The casino appeals to users who want a Canadian online casino with different entertainment options instead of being limited to one category. Its selection includes online slots, table games, live dealer titles, and other popular casino options, making it suitable for users comparing the best online casinos Canada.

One of the main strengths of Lucky7 is its promotional structure. Along with its welcome offer, the casino provides additional rewards such as reload bonuses and cashback opportunities. This makes it a suitable option for users looking for ongoing value rather than only an initial bonus.

Lucky7 also provides a mobile-friendly experience, allowing users to access games, promotions, and account features through smartphones and tablets. The layout is designed for simple navigation, helping users move between different sections without unnecessary steps.

Welcome Bonus & Promotions

- Welcome Bonus: C$3,000 Welcome Bonus + 200 Free Spins

- Saturday Reload Bonus: 100% up to C$2,000 + 100 Free Spins

- Monday Reload Bonus: 100% up to C$2,000 + 100 Free Spins

- Daily Cashback: 20%

- Weekly Cashback: 10%

Key Features

- Wide range of casino games

- Strong promotional options

- Multiple payment solutions

- Cashback rewards for returning users

- Mobile-compatible casino access

- Easy-to-use account management

Our Verdict

Lucky7 performs strongly among the best online casinos Canada because it combines promotional value, game variety, and convenient account features. Its balance of entertainment choices and rewards makes it a suitable option for users who want more than a basic casino experience.

3. Slots Gallery: Best Online Real Money Casino For Slot Variety

Slots Gallery is designed for users who enjoy exploring different types of slot games. In our review of the best online casinos Canada, our experts examined its game selection, promotional offers, mobile performance, and overall usability to understand why it attracts slot-focused users.

The casino places strong attention on reel-based entertainment, offering access to different software providers, classic-style slots, and modern video games with advanced bonus features. This makes Slots Gallery a suitable choice for users searching for the best online real money casino focused on variety and frequent slot promotions.

For users comparing best Canadian online casinos, Slots Gallery stands out because of its extensive slot collection and organised browsing experience. Players can explore different themes, mechanics, and game formats while accessing promotions designed around regular gameplay. Its mobile-friendly design also allows users to browse games, manage accounts, and access promotions through smartphones and tablets.

Welcome Bonus & Promotions

- Welcome Package: Up to $9,750 + 225 Free Spins

- Loyalty Program: Up to 300 Free Spins

- Daily Cashback: Up to 12.5%

- Game of the Month Promotion: Up to 125 Free Spins

- Crypto Bonus: Up to 1 BTC Daily

- Monday Bonus: Up to 100 Free Spins

- Wednesday Bonus: Up to 100 Free Spins

Key Features

- Large slot-focused game collection

- Multiple software providers

- Regular free spin promotions

- Mobile browser access

- Easy game browsing experience

- Different slot styles for various preferences

Our Verdict

Slots Gallery earns its place among the best online casinos Canada because of its strong focus on slot entertainment, accessible design, and wide range of promotional opportunities.

4. Boho Casino: Top Online Casino Canada For Rewards & Promotions

Boho Casino stands out among the best online casinos Canada for users who value regular promotions, cashback opportunities, and a diverse selection of casino games. During our review, our experts evaluated its bonus structure, gaming variety, mobile experience, and overall usability to understand how it compares with other leading casino options.

Unlike casinos that focus only on a single welcome offer, Boho Casino provides multiple promotional opportunities designed for continued engagement. This makes it suitable for users searching for a best online casino Canada experience with ongoing rewards alongside access to slots, table games, and live dealer entertainment.

The casino offers a broad game collection that appeals to different preferences. While slot games remain a major focus, users can also explore table-based options and live casino titles. This variety helps Boho Casino remain a competitive choice among the best Canadian online casinos for users who want flexibility.

Boho Casino also provides mobile-friendly access, allowing users to browse games, manage accounts, and view promotions through smartphones and tablets. The responsive design helps create a convenient experience for users who prefer playing without being restricted to desktop devices.

Welcome Bonus & Promotions

- Welcome Package: Up to $9,750 + 225 Free Spins

- Loyalty Program: Up to 300 Free Spins

- Crypto Bonus: Up to 1 BTC

- Wednesday Bonus: Up to 100 Free Spins

- Monday Bonus: Up to 100 Free Spins

- Daily Cashback: Up to 12.5%

Key Features

- Strong selection of promotional offers

- Cashback rewards for regular users

- Wide range of casino categories

- Mobile-compatible gaming experience

- Multiple payment solutions

- Easy access to bonuses and account features

Our Verdict

Boho Casino performed well in our assessment of the best online casinos Canada because it combines promotional value with a varied gaming experience. Its focus on cashback, loyalty rewards, and regular offers makes it appealing for users who prefer ongoing benefits.

5. BitStarz: Best Real Money Online Casino For Cryptocurrency Payments & Game Selection

BitStarz completes our review of the best online casinos Canada with its extensive game library, flexible payment options, and strong focus on cryptocurrency-friendly gaming. Our experts evaluated BitStarz based on game variety, promotional opportunities, payment flexibility, and overall user experience.

The casino provides access to a wide selection of entertainment options, including online slots, jackpot games, table games, live dealer titles, and original casino games. This makes BitStarz suitable for users searching for the best online real money casino with a broad range of gaming choices.

Among Canadian online casinos, BitStarz is recognised for combining traditional casino entertainment with cryptocurrency payment support. This appeals to users who prefer digital currency options while still wanting access to familiar casino categories.

The casino also provides mobile browser access, allowing users to explore games, tournaments, promotions, and account features from compatible smartphones and tablets.

Welcome Bonus & Promotions

- Welcome Bonus: 300% up to C$2,000 + 180 Free Spins

- Slot Wars: €5,000 Cash Prize Pool + 5,000 Free Spins

- Table Wars: €10,000 Cash Prize Pool

- Originals Tournament: $5,000 Cash Prize

- Monday Reload Bonus: 50% up to C$300

- VIP Cashback Rewards

Key Features

- Cryptocurrency payment support

- Large selection of casino games

- Wide range of gaming categories

- Tournament-based promotions

- Mobile browser compatibility

- Combination of classic and original games

Our Verdict

BitStarz earned recognition in our review of the best online casinos Canada because of its extensive gaming catalogue, payment flexibility, and wide range of entertainment options.

Casino Bonuses and Promotions for Canadians

Bonuses remain an important factor when choosing the best online casinos in Canada. A trusted online casino Canada option should offer clear promotional terms and valuable rewards that enhance the overall gaming experience. The best Canadian online casinos often include a range of offers, such as:

- Welcome Bonuses

Initial rewards for new users after registration and meeting deposit requirements.

- Deposit Match Bonuses

Extra funds added as a percentage of the deposit amount up to a set limit.

- Free Spins

Complimentary spins on selected slot games, giving players additional chances to enjoy popular titles.

- Cashback Offers

A percentage of eligible losses returned during a specific promotional period.

- Reload Bonuses

Additional promotions available for existing users on selected occasions.

- VIP Rewards

Exclusive benefits, bonuses, and loyalty incentives for regular casino users.

Bonus Terms to Know

Before claiming any promotion at the best online casinos Canada, it is important to understand the conditions attached to each offer. Reviewing these details helps users choose an online casino Canada option with fair and transparent bonus rules. Key terms include:

- Wagering Requirement (Rollover)

The number of times bonus funds must be played through before withdrawal (for example, 35x).

- Game Weighting

The contribution different games make toward rollover requirements, with slots often counting at 100% while some table games may contribute less.

- Expiry Window

The time limit available to complete bonus requirements, which may range from a few days to several weeks.

- Max Bet Limit

The maximum stake allowed while using active bonus funds.

- Eligible Games & Deposit Rules

The games that qualify for bonus play and any minimum deposit requirements.

Responsible Gambling

Responsible gambling should always be a priority when using the best online casinos Canada. Real-money gaming should be treated as entertainment, not a source of income. Reliable Canadian online casinos offer tools that help users manage their activity and maintain healthy gambling habits. Key responsible gambling practices include:

- Deposit & Loss Limits: Set spending limits to control your gaming budget.

- Session Timers: Monitor playing time and take regular breaks.

- Self-Exclusion Tools: Temporarily or permanently limit account access when necessary.

- Avoid Chasing Losses: Play within your limits and make informed decisions.

Final Thought

Choosing the best online casinos Canada involves more than searching for the biggest bonuses. Reliable withdrawals, quality game selections, secure payment methods, mobile compatibility, and fair bonus terms all contribute to a better online gaming experience.

Among the reviewed options, Wild Tokyo, Lucky7, Slots Gallery, Boho Casino, and BitStarz stand out as some of the best Canadian online casinos for different preferences. Whether you prefer diverse casino games, rewarding promotions, or flexible payment options, these sites offer different experiences to suit Canadian players in 2026.

Frequently Asked Questions

1. What are the best online casinos Canada players can consider?

Canadian users can consider Wild Tokyo, Lucky7, Slots Gallery, Boho Casino, and BitStarzamong the best online casinos Canada for bonuses, game variety, secure payments, and reliable gaming experiences.

2. Are online casino winnings taxable in Canada?

No, online casino winnings are generally tax-free in Canada for recreational players, as the CRA does not consider gambling proceeds as regular earned income unless pursued as a full-time business.

3. What is the fastest withdrawal method for Canadian players?

Cryptocurrency (Bitcoin, Ethereum, USDT) and e-wallets like MuchBetter offer the fastest cashout speeds, often processing within 0 to 24 hours compared to traditional bank wire transfers.

4. Can I deposit directly using Canadian Dollars (CAD)?

Yes, top online gaming destinations support CAD transactions directly through credit cards, bank transfers, and e-wallets, helping Canadian players avoid unnecessary currency conversion fees.

5. Are mobile casinos popular in Canada?

Yes. Mobile gaming continues to grow, and most leading casino sites provide fully optimized access through smartphones and tablets.