Features

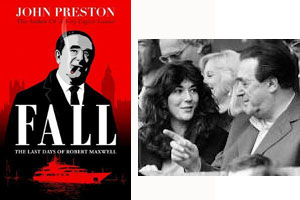

Robert Maxwell was a publishing magnate – and a crook, but what else may he have been?

By BERNIE BELLAN A few weeks back, during one of the weekly bike excursions that a group of men (and occasionally women) go on every Tuesday during the summer, I happened to be talking to one of the members of our group, the ageless Mickey Hoch. (I had profiled Mickey in the April 3, 2019 issue of this paper.)

Mickey asked me whether I knew that there was a new biography out of famed media tycoon Robert Maxwell? When I said that I didn’t know that, Mickey added: “He was my first cousin.”

Robert Maxwell a cousin of Mickey Hoch? Now that was something I just had to find out more about. So, in short order, I bought this latest biography of Robert Maxwell, which is titled “Fall – The Mystery of Robert Maxwell”, by journalist John Preston.

There have been reams of material already published about Robert Maxwell – and although it’s been 30 years since his mysterious death from aboard his yacht, the “Lady Ghislaine”(pronounced Gee-Layn), the escapades of his notorious daughter – the very same Ghislaine, have kept the name Maxwell in the news long after Robert Maxwell’s death.

But to think that Maxwell’s real name was Jan Ludvik Hoch and that he was a first cousin of Mickey Hoch, well – that was something I found so intriguing I just had to dive into this new biography to learn much more about a man who was larger than life in so many respects.

I’m not sure how much more Preston has uncovered in this newest biography of someone about whom so much has been written. Frankly, I had trouble keeping track of all the names that were mentioned throughout the book, often wondering just what was that particular person’s relationship to Maxwell again?

What intrigued me more than anything, however, was Maxwell’s discomfort with his Jewish heritage. For years he disavowed ever having been Jewish, but late in his life he seemed to have done a complete about face and was more than eager to associate himself with his Jewish heritage.

Apparently there were two seminal moments in Maxwell’s life that led to this grand reawakening: One was in 1984, when he was already 61 and was persuaded to go on a trip to Israel for the first time in his life. It was during that trip – and a meeting with then Prime Minister Yitzhak Shamir, that Maxwell decided he was going to become a fervent supporter of the State of Israel. He told Shamir that he was going to become the largest individual investor in the state – and he did, actually investing $50,000,000.

It was also during a visit to Yad Vashem that Maxwell seems to have come to grips with the awful calamity that befell almost his entire family.

Here is how Preston describes that visit: “With his head lowered and his hands plunged into his jacket pockets, he walked through canyons of stone blocks bearing the names of communities that had been wiped out. Stopping in front of one of the blocks, he pointed at the lettering. ‘At the bottom is the shtetl Solotvino where I come from,’ he said. ‘It is no more. It was poor, it was Orthodox and it was Jewish. We were very poor. We didn’t have things that other people had. They had shoes and they had food and we didn’t. At the end of the War, I discovered the fate of my parents and my sisters and brothers, relatives and neighbours. I don’t know what went through their minds as they realized they had been tricked into a gas chamber. But one thing they hoped is that they will not be forgotten …’ Tears welled up in Maxwell’s eyes as he glanced towards the sky. Barely able to speak, he managed to add: ‘And this memorial in Jerusalem proves that.’ Overcome, he walked away.”

Later, Maxwell also paid a visit to his birthplace in Solotvino, which had been part of Czechoslovaki when Maxwell was born, but later became a part of Hungary. Maxwell described his childhood as so impoverished that he was hungry almost all the time.

That impoverished childhood, followed by his managing to escape Czechoslovakia while all but two of his nine siblings – along with his parents, were murdered in Auschwitz, also seems to have traumatized Maxwell for life, although he would never admit it.

And, while reading about Maxwell’s business exploits and his duplicitous nature is certainly interesting, it is the aspect of Maxwell remaking himself into a non-Jew, then making a 180 degree turn the other way that I think most Jewish readers will find most fascinating.

Not only was Maxwell able to adopt a different persona depending upon the occasion, and switch languages with ease (he actually spoke nine different languages), it also seems that he himself had difficulty knowing who exactly he was.

At one point Preston reveals that Maxwell changed his name to DuMaurier, pretending to be French. Why DuMaurier? Because he liked the cigarettes.

As well, Maxwell seems to have been quite fearless. He was decorated with the Military Cross by Field Marshall Bernard Montgomery in 1945 for, among other things, wiping out a German machine gun nest single handedly.

He was also very good looking when he was younger – and quite fit. As the years went on, however, Maxwell’s voracious appetite for food led to his becoming quite obese. As a matter of fact, he was so large upon his death that his coffin could not be fitted into his own private jet and a special plane that is designed especially to carry coffins had to be arranged to take him to Israel, which is where he had wanted to be buried.

Preston interviewed several individuals who described Maxwell’s insatiable appetite. One amusing anecdote is about a lunch that was served in Maxwell’s private dining room at his headquarters. The main course was leg of lamb. Maxwell’s guest that particular day was served first, and he asked for the knuckle of the leg, which was placed on his plate. That guest was momentarily preoccupied by discussing something with another guest who was seated beside him, but when he turned to start eating his meal, he saw that Maxwell had grabbed his own serving from his plate and was proceeding to devour it.

The author suggests that it was Maxwell’s impoverished childhood, when there was never enough food to go around, that led him to develop an insatiable appetite. In fact, according to those who knew Maxwell best, including his wife Betty, he would control himself for the most part when he was with guests in his own home, but later in the evening he would ransack the “larder”. Things got so bad that locks would be put on the larder, but Maxwell’s enormous strength didn’t prevent him from breaking down the door to get at the food.

While Maxwell was certainly a genius at business, helping to build many different companies, including book publishers, newspapers, and the MTV television network, it is not clear what drove him to want to be, as he himself would say, “the world’s richest man”.

Clearly there was an obsession with being accepted by the British Establishment which, while eager to benefit from his business deals, for the most part regarded Maxwell as an “outsider”. It doesn’t seem though that the antagonism that was so often expressed toward Maxwell had much to do with his Jewish roots as Preston does not refer to any antisemitic remarks directed Maxwell’s way.

Ultimately, Maxwell became a fervent supporter of a multitude of Jewish causes, especially the State of Israel. Preston describes a somewhat hilarious scene at Maxwell’s state funeral in Israel when two rabbis physically fought over who was going to be able to mount the podium to deliver a speech praising Maxwell as their prime benefactor.

Yet, there was something else that Mickey Hoch had told me about Maxwell that quite interested me – which was that Maxwell had reputedly worked for the Mossad. The book does reference Maxwell’s helping to arrange the departure of several Jewish “refuseniks” from the USSR, but Preston doesn’t indicae that this had anything to do with the Mossad.

Mickey Hoch (who, by the way, said that he had never met his cousin) also suggested that the Mossad had assassinated Maxwell. There has actually been a book published which makes that claim, but not once in Preston’s book does he even raise that as a possibility.

The book does discuss Maxwell’s incredible network of associates, including the leaders of a great many countries. And, while Maxwell did seem to have had very close associations with a great many dictators, especially behind what was then the Iron Curtain, the notion that has often been raised that Maxwell may also have been an agent for the KGB is given relatively short shrift. (Maxwell did have a close association with Mikhail Gorbachev, also with Boris Yeltsin. At the same time though, Maxwell was twice elected to the British House of Commons as a Labour MP, and seems to have been genuinely appreciative of Western democratic norms.)

Maxwell’s reputation was totally sullied following his death, however, when it emerged that he had ransacked the pension funds of his employees to the tune of £750,000,000. He may not have been the first crook to climb his way to the pinnacle of the business establishment, but he was certainly among the worst.

There has been so much speculation as to whether Maxwell actually jumped off his yacht or simply slipped (apparently he liked to urinate over the side at night, so it’s quite possible that he might have slipped doing that) that it will probably be fodder for more books for years to come.

Still, the question that intrigued me more than anything was the degree to which Maxwell’s impoverished childhood and surviving the Holocaust led him to becoming the legendary businessman – and scoundrel, that he ultimately became. If he hadn’t died under such mysterious circumstances, no doubt he would have spent the rest of his days fending off legal issues related to his brazen skullduggery.

This entire review, I haven’t even mentioned that, of all Maxwell’s nine children, his favourite was Ghislaine. How interesting is it that Ghislaine was the daughter of a financial rogue who was one of the greatest con men of all time, and that she ended up partnering with another notorious rogue, Jeffrey Epstein. No doubt the mysteries surrounding the deaths of both these scoundrels will haunt us for years to come.

Features

K-tip placement at Sets on Corydon

Precision K-Tip placement: Where art meets ultimate hair engineering. ✨

Every strand is custom-blended to achieve seamless movement, zero detection, and absolute freedom (yes, even high ponytails on day one). Precision styling takes patience and technical mastery—the result speaks for itself.

.

Features

Israel pavilion ambassadors – then and now

By BERNIE BELLAN Given that Folklorama is on again and the Israel pavilion – Shalom Square, is in full swing, I thought it timely to resurrect an article I first posted to this website in August 2023.

But before reading that article, I wanted you to see who this year’s ambassadors are for Shalom Square:

It was back in 2023, however, that I set out to answer a question that I had asked our readers to help answer: Where was the very first Israel pavilion located? Some readers had thought it was the Golden Age Club, which used to be located on Pritchard and Salter. But others weren’t so sure. Here then is what I wrote back in August 2023 – when, with the help of a librarian at the Winnipeg Public Library, I was able to solve the riddle of where the first Israel pavilion was located:

It was earlier in August 2023 that I had raised a number of questions about the history of the Israel pavilion at Folklorama.

Among those questions were: Where was the first Israel pavilion located and when did the Israel pavilion actually become a permanent fixture in the YMHA on Hargrave (before moving to its current home in the Asper Campus)?

As part of my search for answers to those questions I turned to David Cohen, who had long been the coordinator of the Israel pavilion when it was located on Hargrave, but who didn’t step into that role until 1975.

David thought that the Israel pavilion hadn’t moved to Hargrave until 1974, but he wasn’t sure where the first Israel pavilion had been located.

I tried to find information using the Winnipeg Public Library online digital archive. In case you didn’t know, anyone with a library card can access the library’s online archive. You can also have access to newspaperarchive.com through the library’s digital archive. Newspaperarchive.com is an invaluable reference tool for journalists especially – or anyone wanting to access old newspaper archives, for that matter, but ordinarily you would need a subscription to newspaperarchive.com in order to use it. For some reason, however, the search function in the Winnipeg Public Library’s digital search engine didn’t produce results when I entered the word “Folklorama.”

As a result I called the Winnipeg Public Library for assistance and received great help from someone by the name of Louis-Phillipe. After taking my information, Louis-Phillipe phoned me to say that he had found out that the library had compiled a file of press clippings related to Folklorama going back to the very first year, 1970.

Further, Louis-Phillipe said, he had found a list of the 22 pavilions in that first year of Folklorama, along with where they were located. It turns out that the Israel pavilion was actually located in two different venues that first year: the Rosh Pina and the Shaarey Zedek.

The next day I also heard from reader Phyllis Dana, who confirmed that the Israel Pavilion had been in both synagogues. Phyllis also remembered that the only food served that first year was honey cake.

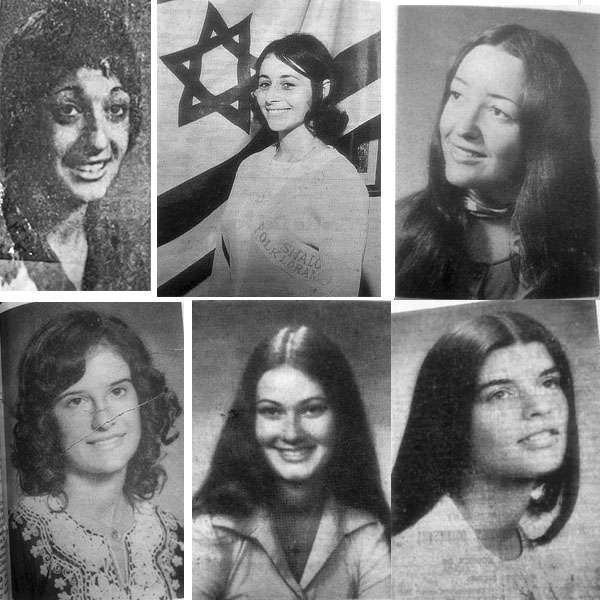

But the pièce de resistance came when I heard from reader Marilyn Breitman (née Stitz), who now lives in Calgary, when she phoned me on Monday, August 21 (which is when she received the August 16 issue of the paper with my story about Folklorama).

Marilyn told me that, not only did she remember that the first Israel pavilion alternated between the Rosh Pina and the Shaarey Zedek, she had actually been the female representative of the Israel pavilion that first year. Her title, Marilyn said, was simply “Jewish.”

But, as you might also recall, the entire confusion over where the first Israel pavilion was located began with an email I had received from Roz Greenfeld, who had written to correct my mistake when I had written in the August 2 issue that the Israel pavilion had been located in the YMHA from the very beginning.

Roz pointed out that, in 1971, the second year of Folklorama, the Israel pavilion was located in “Council House” or, as it was better known, “The Golden Age Club,” on Pritchard and Salter. How did she remember that? Roz was the female representative of the pavilion that year. Her title, as I found out was “Miss Judea,” she said.

So, if the Israel pavilion was located at both the Rosh Pina and Shaarey Zedek in that first year of Folkorama, and in the Golden Age Club that second year, where was it after that?

It was left to Jewish Heritage Centre of Western Canada archivist Andrew Morrison to come up with the answer to that question. Andrew informed me that the Israel pavilion did indeed move to the YMHA in 1972 and remained there for the next 25 years, until it moved to the Asper Campus in 1997.

There was a further footnote to the story, which is when I decided to try my luck with the Winnipeg Public Library’s online archive one more time. This time, rather than searching for “Folklorama,” I tried searching for old copies of both the Free Press and the Tribune from August 1970. I did manage to get results for the Tribune and when I entered a specific search within the Tribune I found a picture of all the famale representatives of pavilions – in bathing suits.

It turned out – and this was corroborated by both Marilyn Breitman and Roz Greenfeld, the female representatives had to parade in unison – in bathing suits, as part of Folklorama festivities. Each year, as well, a queen of Folklorama was chosen. Neither Marilyn nor Roz was made queen, both of them told me, although Roz was voted “Miss Congeniality.”

In addition to finding out about the early days of the Israel pavilion, I also learned that the Chai dancers were not regular performers at the Israel pavilion in those early years – as they eventually did become. Chai performers would dance only one night in those first years, with other entertainment the other nights.

I did enlist Andrew Morrison’s help once again and did find that Chai performed only one evening during the first few years of Folklorama – from 1970 to 1976. In 1977 Chai began performing every night of Folklorama, but there were other performers on hand as well, including Jerry Maslowsky and Rabbi Yosel Rosenzweig. In 1978 the Chai Folk Ensemble was the featured entertainment every evening; however, a notice that appeared in our paper did say that whistler Harvey Pollock would “be on hand” to entertain – whatever that meant.

While some may wonder of what earth shaking importance all this is, I ask: Isn’t it fun to look back in time – for just a little while, instead of worrying about more immediate problems, such as global warming, inflation, terrorist attacks in Israel, and whether Donald Trump will be president while he’s in jail?

Features

EINSTEIN, RITA AND ME

By DAVID R. TOPPER In the early 1960s, when I was an undergraduate student majoring in Physics at Duquesne University in Pittsburgh – there was only one girl in my advanced physics classes. As I learned later, nothing much had changed since the days of Einstein. When he was studying Physics at the Polytechnic in Zurich, the physics classes were all male – except for Mileva Marić, a Serbian who was the first girl in high school ever to take a physics course in the entire Austro-Hungarian Empire. Because Switzerland was the only place where women were admitted to university classes, she was there with Albert in Zurich.

She was very smart, especially in math, and also proficient at the piano. Born with a dislocated hip, Mileva had a slight limp, and the men in the class ignored her – except for one, Albert. They became a couple and eventually married.

Back to me in my university physics classes – where it seems that little had changed for over sixty years. In my advanced classes there was only one girl. Her name was Rita. She mainly stayed to herself. Majoring in Mathematics, she took all the advanced physics courses available, right through the fourth year. In short, in those predominantly male classes, she was an anomaly – alone and ignored by her classmates.

Except me. No, I didn’t date her, yet I didn’t ignore her. During those undergraduate years, I lived at home and took a bus or a trolley to school five days a week, leaving early in the morning. The university is in downtown Pittsburgh. Walking to the campus, I first went to the Physics Department, using it as my base. From there I went to my other classes during the day. There was a small classroom in the Department that was almost always empty, especially in the morning. It could be used for individual studying or small group discussions and such. In the early morning, I was usually the only one there – except for Rita, who used it for studying, too. She often was there, even before me. Usually the conversation started by me saying something like: “Hi Rita, did you get the last problem in mechanics class homework?” Her response was invariably, “Yes.” We would go over it, with her finding my mistakes. We had an amiable relationship that never went beyond our interactions about physics – right up to the end of our university years. As far as I can remember, I don’t think I knew much about her beyond the classroom.

But one event, which I’ll never forget, stands out. It was during our last year of classes in a course on the theory of relativity. For the textbook the prof used a paperback edition of the original papers on the theory. Early in the course, we went through Einstein’s first paper of 1905 – step by step. On this particular day, the prof came in and said he had a problem with the next step in the paper. As we all sat with our books in front of us, he pointed to a certain equation where we ended in the previous class. In the next sentence, Einstein says that such and such follows. The problem for the prof was that he didn’t know how Einstein got that deduction. I looked at it, and didn’t have a clue either.

Just then, Rita’s hand went up. She said she thinks she knows how Einstein got it. The prof asked her to come up to the blackboard and show him. Rita did, and the prof said that she was right. I’m quite sure that – then and there – Rita got an A in that course, if not an A+.

That gives you some idea about Rita and my relationship with her at the time. Not a very significant part of my 4-year undergraduate years – except for this one event in a physics course.

Why then am I bringing this up now, so many years later? Here’s why.

I graduated with my BS degree in the fall of 1964. I then went to graduate school at Case Institute of Technology in Cleveland, majoring in Physics. (It’s now Case-Western Reserve University.)

When I moved there, I lived in a formerly swanky hotel on the edge of the campus, which was purchased by the university as a residence solely for graduate students. They called it The Graduate House. Eleven floors, the top 8 with suites for students, with one floor solely for female students. It was a radical experiment in co-ed living for the time.

My first day there, after getting my room and putting my things in drawers and so forth, it was late in the afternoon – and I was hungry. I had been told when I registered that the dining hall would open the following morning, but for now there was no food. However, on the third floor there were vending machines with sandwiches and such, so I went to find them.

Going down the elevator, exiting at the third floor, and walking down a hall – suddenly I heard my name called. “David, what are you doing here?” Turning around – there was Rita! It was quite a surprise for both of us. This tells you how minimally we interacted before; not even knowing that we both were going to the same graduate school.

I told her that I was majoring in Physics at Case. She, of course, was majoring in Math. After a chat about all this, I said that I was looking for the sandwich machines. She said that there was a diner nearby, and she was going there for dinner with someone else she had just met so I went, too. Thus, Rita and I reunited in Cleveland, now living in the same building.

In a short while, I made friends with a group of people in the Graduate House with diverse majors. Some were in various sciences, others in humanities. It was a lively group, with animated discussions on a range of academic topics, including politics, especially as the Vietnam War became the center of the news in the USA.

Rita was not a part of that group, but I did often see her. Being the eager student that I was, I was up early, getting to the university to study in the library before classes started. Coming to the dining room for breakfast, not long after it opened, I often saw Rita, too – all alone in a far corner. I took my tray and we had breakfast together. Except for that morning ritual, I seldom had any interactions with her.

Thinking about this now, I find the parallel morning rituals (first in Pittsburgh and then in Cleveland) a fascinating serendipitous episode in my life. The difference was that in Cleveland, we were not taking the same courses so we didn’t have to compare solutions to homework. We did talk about our respective courses, and interestingly a parallel appeared. By around mid-term of that first year in graduate school, we both were less than enthusiastic about what we were learning and, accordingly, were both thinking of not carrying on in our respective subjects.

For me it was Quantum Mechanics and the impossibility for us to know reality in itself. Everything was statistical, uncertain and almost esoteric. I found the uncritical attitude toward this world-view to be almost religious in nature. (I only learned later that Einstein felt the same way!)

For Rita, it was the same, despite the different fields. The math now was far beyond basic geometry, algebra and calculus. Topology, Group Theory, Galois’ Theory, and more – all culminating in Gödel’s Theorem, which asserts that all mathematical knowledge is inherently incomplete. It all was too esoteric for her. She knew that she was not going to get a PhD in mathematics.

We commiserated together, with another parallel in our unusual relationship, but with a difference. I still wanted to get my Master’s Degree and somehow still go on to get a job as a professor – that had been my goal in life ever since my first semester at Duquesne. Rita, however, was thinking of dropping out immediately and leaving university life altogether.

For me, this problem was resolved in my second year of Physics at Case, when I took a course taught by Martin Klein. Although he was a physicist in the Department, for many years he no longer was doing research in it. Instead, he was writing papers on the history of the subject – mainly involving Einstein, Boltzmann, Gibbs, Ehrenfest and others. Today those papers are paragons in the field. It was my extremely good luck that the department permitted him to teach such material for the first time.

I loved the course. I was enthralled by the topics – this was the way I wanted to learn physics, through its history. After getting my Master’s in Physics at the end of that year, I moved across campus to the History of Science Department. In another four years I had a PhD in the subject.

Back to early 1965: I tried to talk Rita out of dropping out, but she was adamant. The kicker was this: she really preferred numbers with $$$$ in front of them. Yes, she wanted to be an accountant. She didn’t want to waste any more time here, when she could be home getting her accounting credentials. As I recall, sometime before the spring of that year she went back to Pittsburgh. I’m sure she had an easy time getting her accounting licence and all that went with it. As she was very smart. My guess is that she was an excellent accountant and was very successful in that career.

I have no way of knowing. We didn’t keep in touch (honestly, I don’t know why not) and I can’t even remember her last name. All that I can recall is what I’ve written here. Nonetheless, I find these two interactions between Rita and me an interesting and pleasing tidbit about life and relationships – so much so that I deem it worthy of repeating here.

David R. Topper writes in Winnipeg, Canada. His work has appeared in Mono, Poetic Sun, Discretionary Love, Poetry Pacific, Academy of the Heart & Mind, Altered Reality Mag. and elsewhere.

His poem Seascape with Gulls: My Father’s Last Painting won first prize in the annual poetry contest of CommuterLit Mag – May 12, 2025.